分析:评估与结果分析

简介

分析 旨在展示 日内交易 的图形报告,帮助用户以可视化方式评估和分析投资组合。以下是可查看的一些图形:

- analysis_position

report_graph

score_ic_graph

cumulative_return_graph

risk_analysis_graph

rank_label_graph

- analysis_model

model_performance_graph

Qlib 中所有累积收益指标(如收益、最大回撤)均通过求和计算,以避免指标或图表随时间呈指数偏斜。

图形报告

用户可以运行以下代码获取所有支持的报告。

>> import qlib.contrib.report as qcr

>> print(qcr.GRAPH_NAME_LIST)

['analysis_position.report_graph', 'analysis_position.score_ic_graph', 'analysis_position.cumulative_return_graph', 'analysis_position.risk_analysis_graph', 'analysis_position.rank_label_graph', 'analysis_model.model_performance_graph']

注意

更多详细信息,请参阅函数文档:类似 help(qcr.analysis_position.report_graph)

用法与示例

analysis_position.report 的用法

API

图形结果

注意

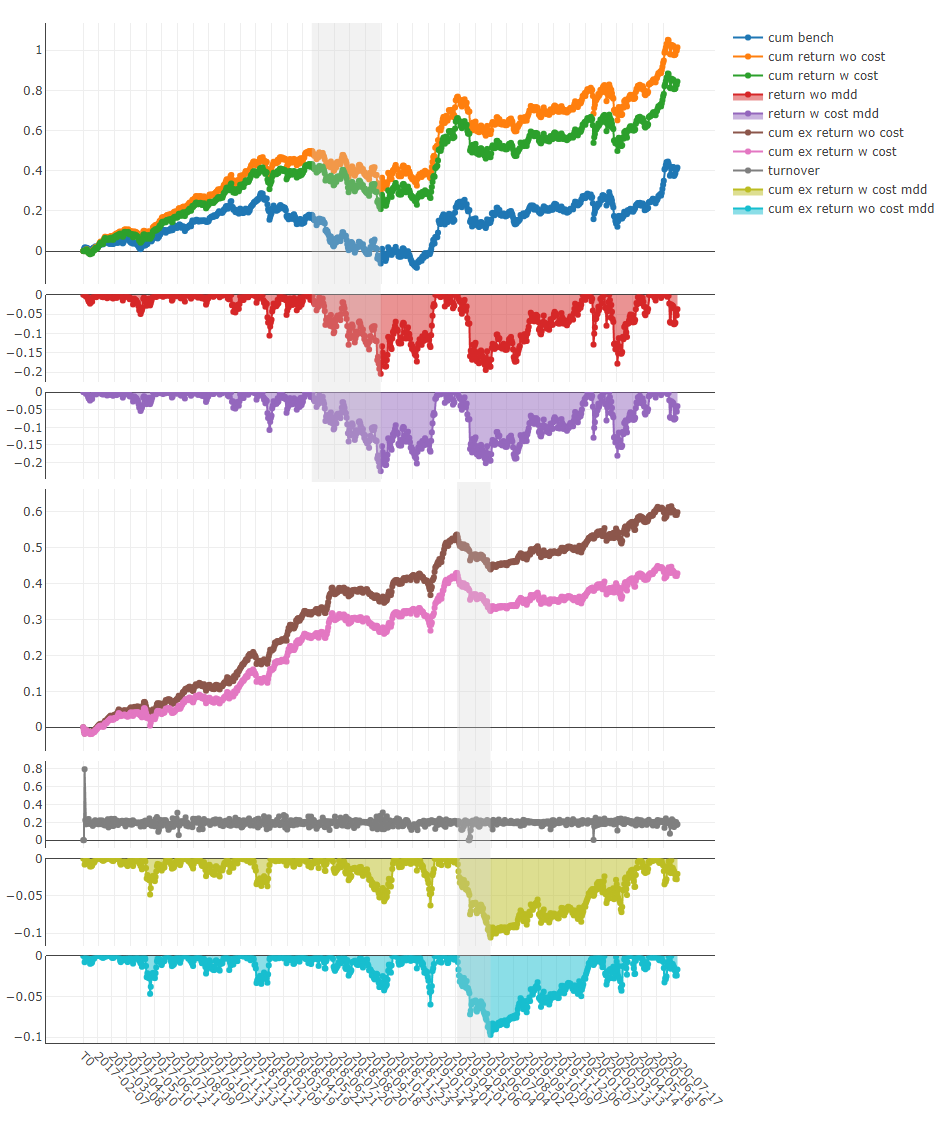

X 轴:交易日

- Y 轴:

- cum bench

基准的累积收益序列

- cum return wo cost

不考虑成本的投资组合累积收益序列

- cum return w cost

考虑成本的投资组合累积收益序列

- return wo mdd

不考虑成本的累积收益最大回撤序列

- return w cost mdd:

考虑成本的累积收益最大回撤序列

- 无成本累积超额收益

投资组合与基准相比的无成本累积异常收益(CAR)序列。

- 有成本累积超额收益

投资组合与基准相比的有成本累积异常收益(CAR)序列。

- 换手率

换手率序列

- 无成本累积超额收益最大回撤

无成本累积异常收益(CAR)的回撤序列

- 有成本累积超额收益最大回撤

有成本累积异常收益(CAR)的回撤序列

上方阴影部分:对应于 无成本累积收益 的最大回撤

下方阴影部分:对应于 无成本累积超额收益 的最大回撤

使用 analysis_position.score_ic

API

图形结果

注意

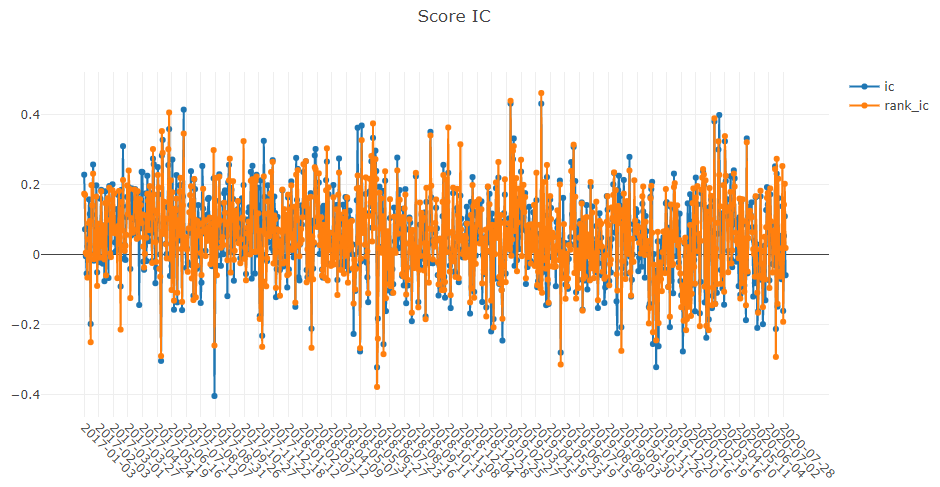

X 轴:交易日

- Y 轴:

- ic

标签 与 预测得分 之间的 皮尔逊相关系数 序列。在上例中,标签 定义为 Ref($close, -2)/Ref($close, -1)-1。更多详情请参阅 数据特征。

- rank_ic

标签 与 预测得分 之间的 斯皮尔曼等级相关系数 序列。

使用 analysis_position.risk_analysis

API

图形结果

注意

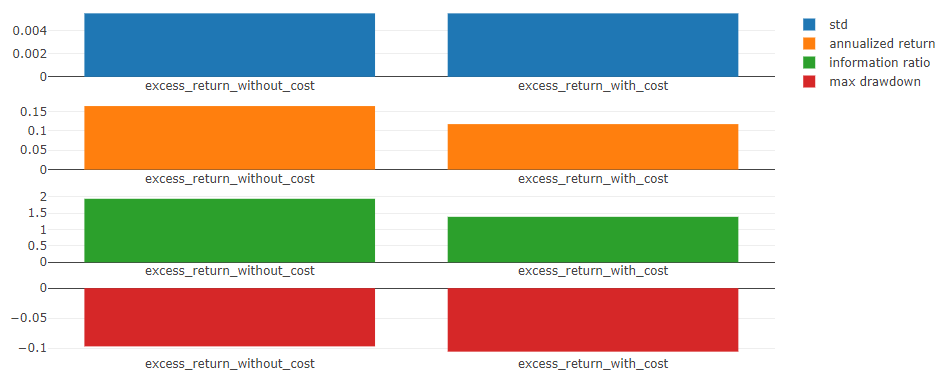

- 通用图表

- std

- 无成本超额收益

无成本累积异常收益(CAR)的 标准差。

- 有成本超额收益

有成本累积异常收益(CAR)的 标准差。

- 年化收益

- 无成本超额收益

无成本累积异常收益(CAR)的 年化收益率。

- 有成本超额收益

有成本累积异常收益(CAR)的 年化收益率。

- 信息比率

- 无成本超额收益

无成本的 信息比率。

- 有成本超额收益

有成本的 信息比率。

欲了解更多关于信息比率的信息,请参阅信息比率 – IR。

- 最大回撤

- 无成本超额收益

不考虑成本的CAR(累计异常收益)的最大回撤。

- 有成本超额收益

考虑成本的CAR(累计异常收益)的最大回撤。

注意

- 年化收益/最大回撤/信息比率/标准差图表

X 轴:按月分组的交易日

- Y 轴:

- 年化收益图表

- 不考虑成本的年化超额收益

不考虑成本的月度CAR(累计异常收益)的年化收益率序列。

- 考虑成本的年化超额收益

考虑成本的月度CAR(累计异常收益)的年化收益率序列。

- 最大回撤图表

- 不考虑成本的最大回撤超额收益

不考虑成本的月度CAR(累计异常收益)的最大回撤序列。

- 考虑成本的最大回撤超额收益

考虑成本的月度CAR(累计异常收益)的最大回撤序列。

- 信息比率图表

- 不考虑成本的信息比率超额收益

不考虑成本的月度CAR(累计异常收益)的信息比率序列。

- 考虑成本的信息比率超额收益

考虑成本的月度CAR(累计异常收益)的信息比率序列。

- 标准差图表

- 不考虑成本的最大回撤超额收益

不考虑成本的月度CAR(累计异常收益)的标准差序列。

- 考虑成本的最大回撤超额收益

考虑成本的月度CAR(累计异常收益)的标准差序列。

使用analysis_model.analysis_model_performance

API

图形结果

注意

- 累计收益图表

- 组 1:

累计收益序列(标签的排名比例 ≤ 20%的股票组)

- 组 2:

股票组的累计收益系列(20% < 标签的排名比例 ≤ 40%)

- 第 3 组:

股票组的累计收益系列(40% < 标签的排名比例 ≤ 60%)

- 第 4 组:

股票组的累计收益系列(60% < 标签的排名比例 ≤ 80%)

- 第 5 组:

股票组的累计收益系列(80% < 标签的排名比例)

- 多空:

第 1 组与第 5 组的累计收益之间的差值系列

- 多-平均

第 1 组的累计收益与所有股票的平均累计收益之间的差值系列

- 排名比例可表示为如下公式。

- \[排名比例 = \frac{标签的升序排名}{投资组合中的股票数量}\]

注意

- 多空/多-平均

每个交易日多空/多-平均收益的分布

注意

- 信息系数

投资组合中股票的标签与预测得分之间的皮尔逊相关系数系列。

图形报告可用于评估预测得分。

注意

- 月度 IC

信息系数的月度平均值

注意

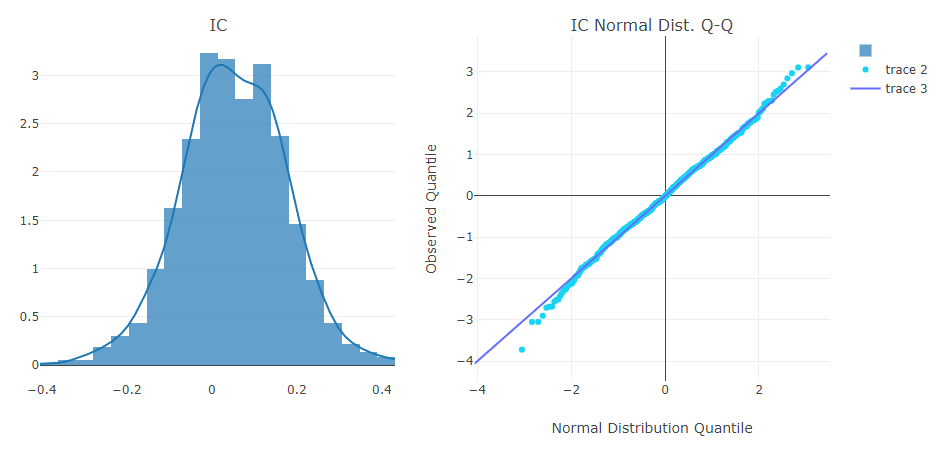

- IC

每个交易日信息系数的分布。

- IC 正态分布 Q-Q 图

分位数-分位数图用于展示每个交易日信息系数的正态分布情况。

注意

- 自相关

每个交易日投资组合中股票的最新预测得分与lag天前的预测得分之间的皮尔逊相关系数系列。

图形报告可用于估算换手率。